Equity markets around the world followed a very similar pattern this year. Every individual index chart shows an aggressive drop in early April, caused by Liberation Day, followed by a V-shape recovery aligned with Trump’s rollback of his aggressive new tariff policy.

Following that bout of volatility, almost all markets continued to rise to new record highs throughout the year. It’s only a matter of how much.

And the difference across markets is notable. Considering all the talk about an AI bubble and concentration risk centered around the Magnificent 7, it’s somewhat surprising that the US market has actually lagged most of its peers in 2025. Or perhaps it has lagged exactly because of these concerns as investors have sought better opportunities and lower risk elsewhere.

Major markets in Asia, Europe and South America all outperformed the US. So did precious metals which had an absolutely insane year. Add a considerably weaker dollar on top of that and foreign investors would have been way better off investing outside of the US in 2025.

Just take a look at all the stats below.

Equities

America

🇺🇸 S&P 500 saw a 21% pullback in the spring, bottoming out after Liberation Day in April, and still managed to close the year with a very respectable 16.39% gain. This comes on the back of +24% and +23% gains in 2023 and 2024.

🇺🇸 Nasdaq Composite closed the year 20.36% higher after following a similar pattern as the S&P, albeit with somewhat higher beta.

🇺🇸 Dow Jones Industrial ended 2025 12.97% higher and perfectly in line with the 13.7% and 12.88% gains recorded the two years before.

🇺🇸 Russell 2000 continued to lag its big brothers with a modest 11.29% gain in 2025.

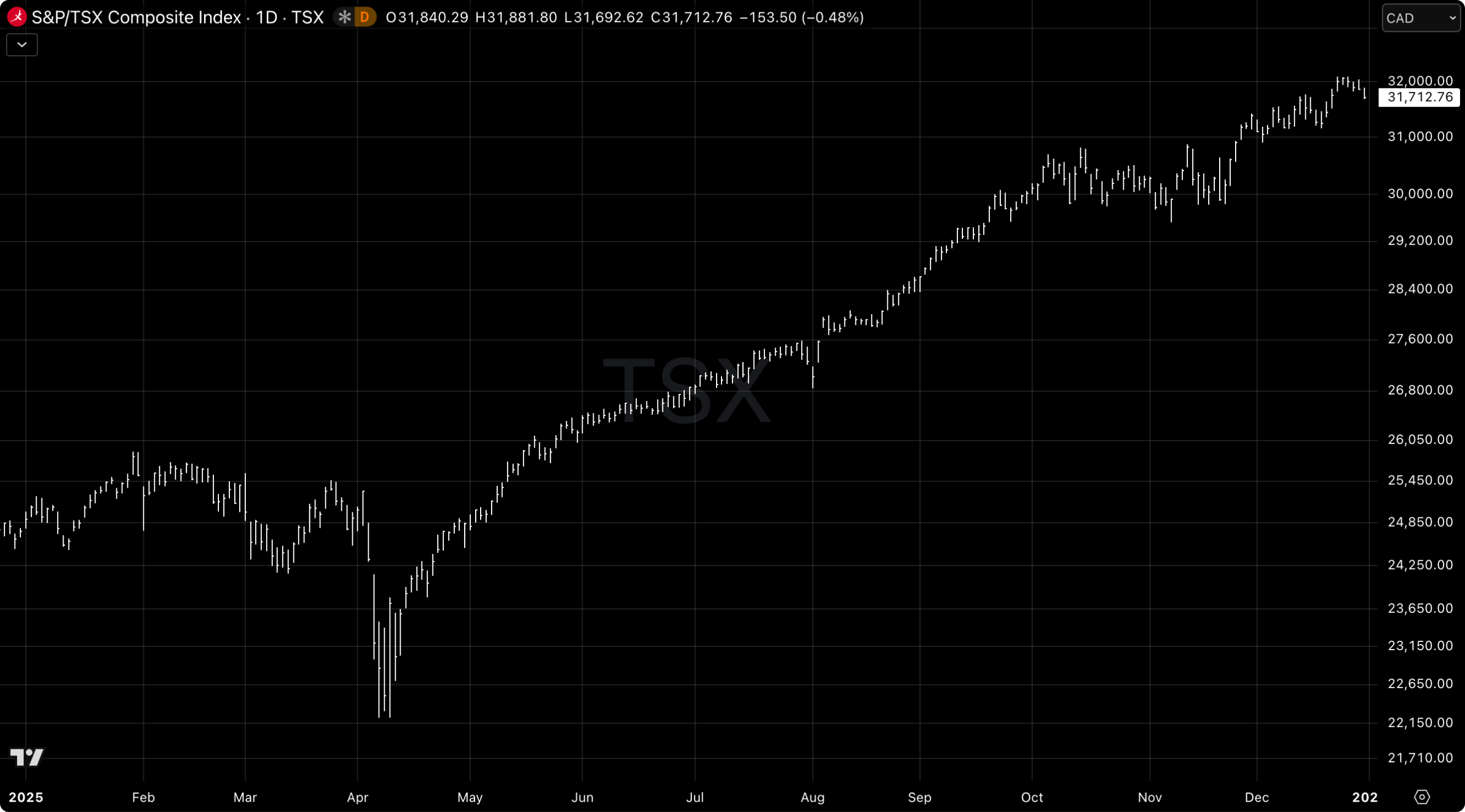

🇨🇦 TSX had one of the most steady, impressive runs from May through September and closed with a 28.25% gain for the year.

🇲🇽 IPC rallied almost 30% in 2025 despite ongoing trade tensions with the US. Notably, this strong year came on the back of a 13.72% decline in 2024.

🇧🇷 Bovespa fell more than 10% in 2024 but delivered a strong comeback in 2025 by surging 33.95%.

🇦🇷 Merval declined more than 42% from January to the bottom in September and yet closed 2025 with a 20.44% gain. The year included a 21.77% single-day jump on the back of Milei’s midterm election victory in September. Wild year for Argentina.

Europe

🇪🇺 STOXX 600 had a strong year and actually ended up outpacing the S&P 500 with a 16.66% gain. Both Germany and multiple South- and Eastern European markets saw outsized gains.

🇬🇧 FTSE 100 surged 21.51% in 2025 for its best year since the post-GFC rebound in 2009. The rally came amid concerns over an economic slowdown and sticky inflation, offset by an accommodative government and central bank.

🇩🇪 DAX closed 2025 with a strong 23% gain but the performance was very unevenly distributed. In fact, all of the action happened in the first five months of the year. The index started out by rallying 17.5% on the back of a rally in defense stocks before topping out in March and getting slammed back down by Trump’s tariff rollout. After a V-shaped recovery from a 21% drop, it extended its year-to-date gain to 22% in May and has basically gone sideways ever since.

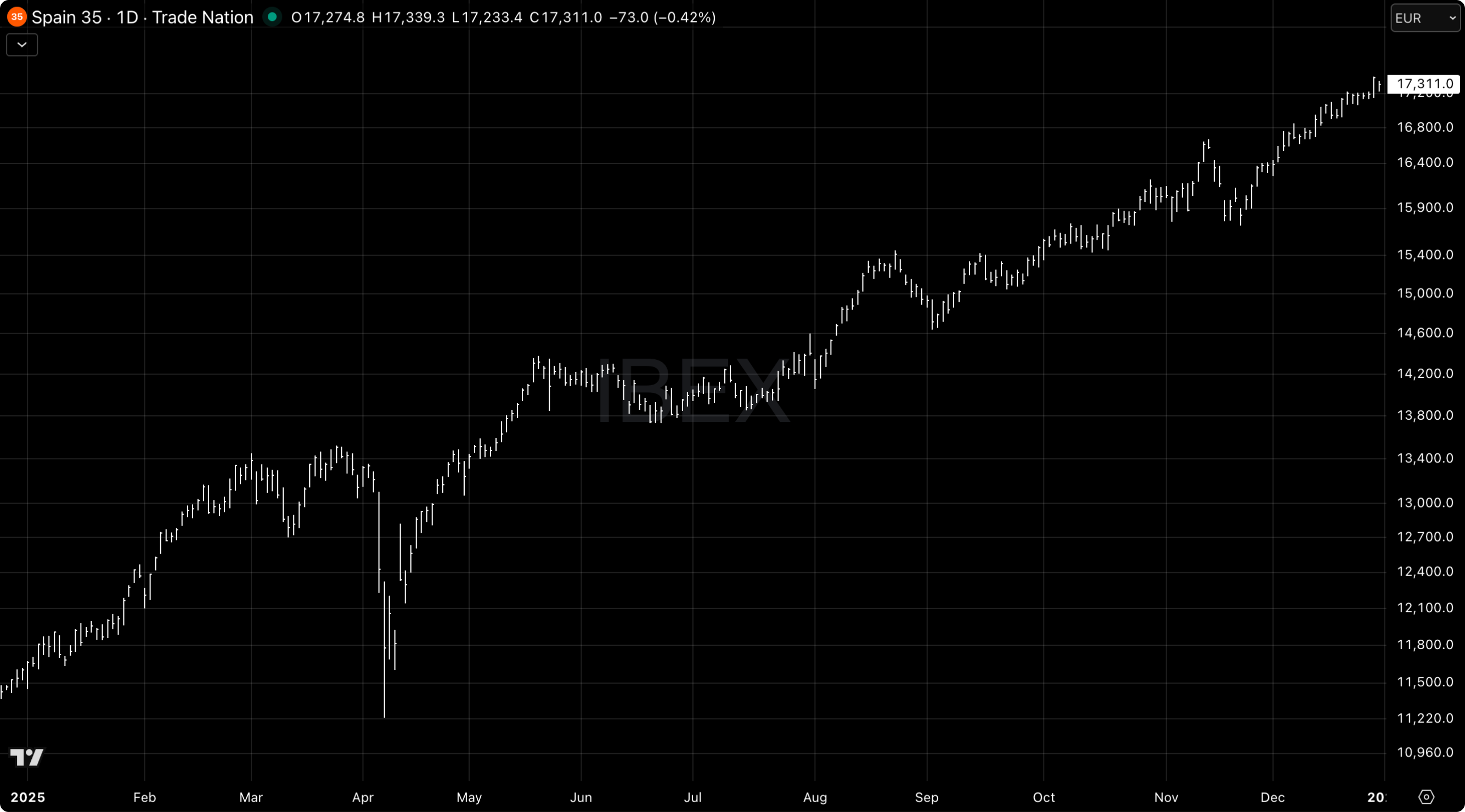

🇪🇸 IBEX 35 soared 49.2% for the year and more than 53% from the Liberation Day lows. The Spanish index ended up as one of the top performers in Europe, driven by massive gains in financials like Banco Santander, BBVA, and CaixaBank which surged 126%, 112%, and 99% respectively.

🇫🇷 CAC 40 rose 10.42% in 2025 amid more political turmoil. The index is bumping up against the 8,260 level that served as resistance on multiple occasions over the past two years. A breakout could be a strong buy signal.

🇮🇹 IT40 also had a great year, rallying 31.23% for its best performance since the index was created in 2011.

🇩🇰 C25 was the big laggard in Europe in 2025 and only narrowly closed out in the green. The index pulled back around 20% in the spring like most other indexes but failed to rebound like the rest. The biggest drag on the index was Novo Nordisk who lost 47.89% of its value in 2025.

Asia

🇯🇵 Nikkei 225 was down more than 23% for the year when it hit the bottom in April after Liberation Day. It quickly recovered most of the losses but remained in negative territory until July when it went on an epic run and rallied 25% in four months. The Nikkei closed the year above 50,000 for the first time after a 26.18% gain.

🇨🇳 Hang Seng kicked off the year with a brief pullback before surging to a 24% year-to-date gain in March. It then gave it all back when Trump initiated his trade war and took aim at China in particular. The Hang Seng plummeted more than 13% on April 7 alone when it reopened after Liberation Day. It had recovered all of its losses by July and held up alright through to year end, closing with a 27.77% gain for 2025. It’s now “just” 30% away from reclaiming its all-time high reached in 2018. If momentum continues into 2026, this could be the year.

🇮🇳 Nifty 50 continued its slide into 2025 after topping out in September of 2024. It was down 7% for the year in early March before staging a rebound, only to get slammed back down to new local lows in early April. The Nifty 50 only saw modest gains after recovering from Liberation Day and was one of the few big indexes that underperformed the S&P 500, closing out the year with a 10.51% gain. Meanwhile, the Indian rupee also weakened by 5% against the USD, bucking the general dollar trend of 2025 and closing at its lowest level on record.

🇰🇷 KOSPI was the clear winner of 2025 and even outperformed gold with a 75.63% surge. It rallied 40% in three months after Liberation Day, paused for two months, then soared another 32% to its peak in early November. The rally was largely driven by massive gains in the largest components of the Kospi index, Samsung and SK Hynix. The two heavyweights surged 125% and 274% respectively.

🇹🇼 TSEC plummeted 27% from high to low in early 2025 before recovering and closing the year with a 25.74% gain. This marked the third straight year of +25% gains for the Taiwanese index.

Currencies

💰 The DXY rallied into Donald Trump’s election victory and inauguration day in January but basically topped out at 110 when he took office. It then plummeted to sub-97 in the summer before stabilizing. It closed the year at 98.28, down 9.4% for its worst year since 2017 and 2nd worst since 1990. The Trump administration has been actively pursuing a weaker dollar which helps out US companies as well as the country at large when doing business internationally.

🇪🇺 USD.EUR almost hit parity when it topped out at 0.982 in January before starting its decline and closing the year almost 12% weaker at 0.851 EUR.

🇬🇧 USD.GBP held up a little better than the USD index at large with a 7.12% decline in 2025.

🇯🇵 USD.JPY closed the year just 0.29% lower than where it started but was arguably one of the most noteworthy and talked-about currency pairs in 2025. It topped out above 158 in January, close to the level where the BoJ stepped in and intervened in the summer of 2024, contributing to the massive yen carry trade unwind back then. After a steep 12% decline, the USD again started rallying against the yen in April and strengthened through to year-end before closing virtually where it started after another rollercoaster of a year.

🇨🇳 USD.CNH initially held up better than the USD at large. However, as the dollar overall stabilized over the summer, it escalated its weakening against the Chinese yuan and closed at the lows of the year after a 4.9% decline.

Commodities

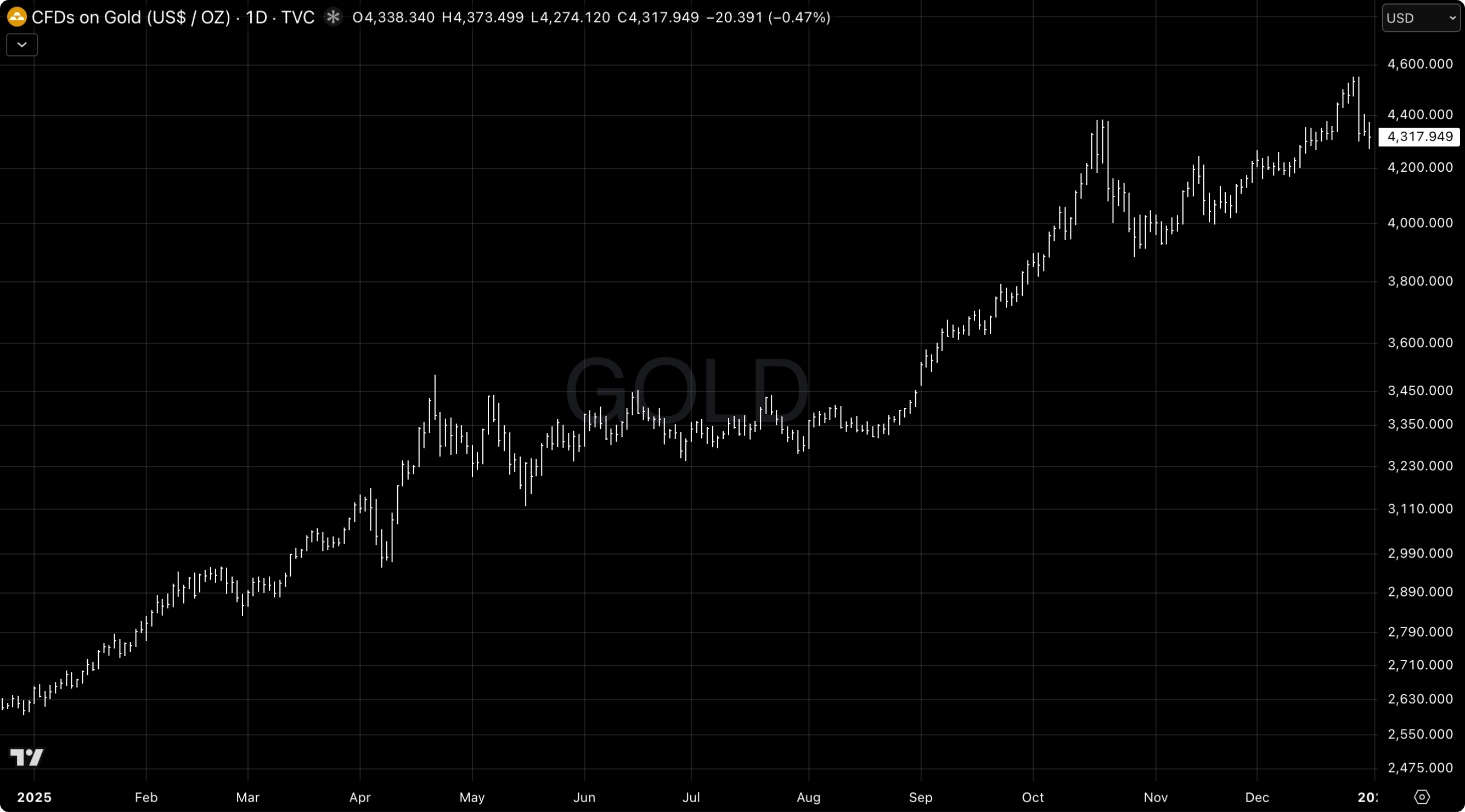

🥇 Gold had a wild 2025, soaring 64.55% for its best year since 1979. The price of gold has now more than doubled in just two years and currently sits at $4,318 per ounce. Gold won as a debasement hedge and flight to safety in a world with more geopolitical instability. Arguably coupled with a healthy dose of speculation and fomo as the price kept going up and up.

🥈 Silver finally surpassed the $50 level where it topped out in 1980 and 2011. The breakout happened in October when silver was already up more than 80% year-to-date. After a brief pullback, it surged to $84 on December 29th before pulling back from what could seem like a blowoff top. However, even after a 14% pullback, silver finished 2025 with a 147.88% gain and earned the title as chart of the year (in my book).

🥉 Copper had what would typically be considered a stellar year, surging 41.61% to a new all-time high of $5.71 per ounce. It does somewhat pale in comparison to gold and silver though. Perhaps copper will play catch-up in 2026? I’m long a basket of precious metals and continue to cheer for all of them to win.

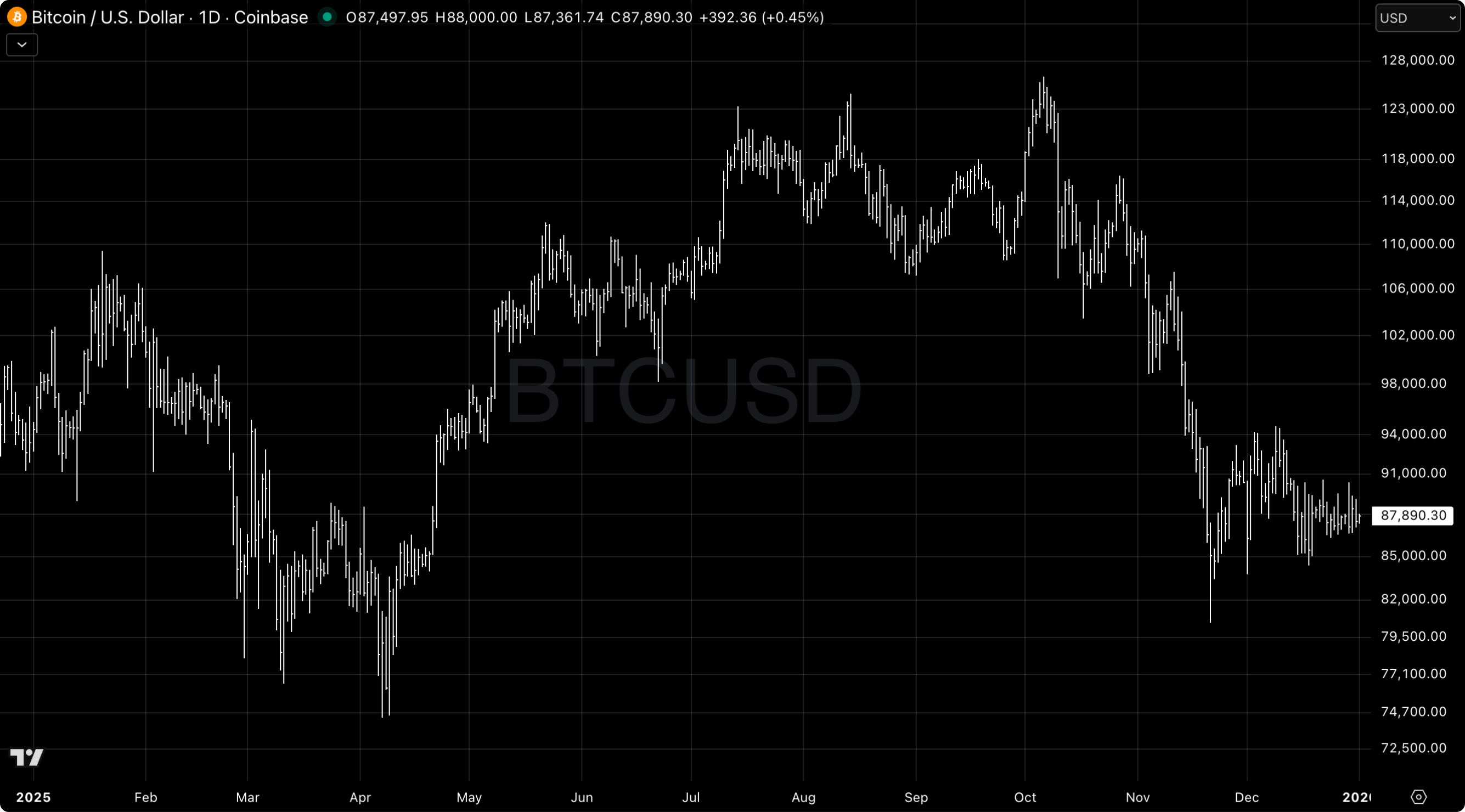

🏆 Bitcoin was easily one of the biggest disappointments of the year. In the face of a much more favorable regulatory landscape and with the self-proclaimed crypto president leading the US, Bitcoin actually managed to fall 6.27% in 2025. It opened the year around $93k, fell to $74k in April, rallied to new record highs above $126k in the fall, and then declined from there. It closed out 2025 at $87.5k. Large, long-term holders have been behind most of the selling into year-end, perhaps just following the 4-year cycle playbook that has worked so well over the past decade. If Bitcoin reaches a new all-time high in 2026, that pattern is officially broken. Fingers crossed.

Bond yields

The Japanese bond market was the big story of 2025, ripping to new all-time highs admits the BoJ's rate hiking cycle. Both the US and Europe saw a significant yield curve steepening as rates kept coming down while growth and inflation expectations went up.

🇺🇸 The US 2-year yield fell along with the Fed’s rate-cutting cycle, closing the year at 3.475% after an 18% decline.

🇺🇸 The US 10-year yield declined 8.97% and closed the year at 4.163%.

🇺🇸 The US 30-year yield reacted more to expectations for both higher growth and inflation, inching up by 1.15% for the year and closing out at 4.841%.

🇪🇺 The Euro 2-year yield initially fell but stabilized and went higher as the ECB’s rate-cutting cycle slowed and essentially came to an end. The 2-year yield rose 1.19% in 2025 and closed at 2.12%.

🇪🇺 The Euro 10-year yield soared 20.38% as rate cut expectations fell while growth and inflation prospects rose. It closed at 2.847% after bottoming out around 2.3%.

🇨🇳 The China 10-year yield hit record lows early in the year but rallied to close 10.83% higher at 1.862%.

🇨🇳 The China 30-year yield followed a similar pattern as the 10-year, surging 19.84% for the year and closing at 2.313% after hitting new lows around 1.8%.

🇯🇵 The Japan 2-year yield soared 93.88% in 2025, albeit from an extremely low base. It started out at 0.6% and closed at 1.168%, its highest level on record, as the BoJ continued to raise rates to combat sticky inflation.

🇯🇵 The Japan 10-year yield jumped almost 90% to a new all-time high above 2%.

🇯🇵 The Japan 30-year yield surged 49.5% and closed the year above 3.4%. Prior to this, the record high for the Japan 30-year yield was the 2.6% it traded at before the GFC. Japan’s bond yields were a major story in 2025.

.png)