The US overtakes Europe, Japan and China continue to rally, and the dollar continues to slide.

Equities

America

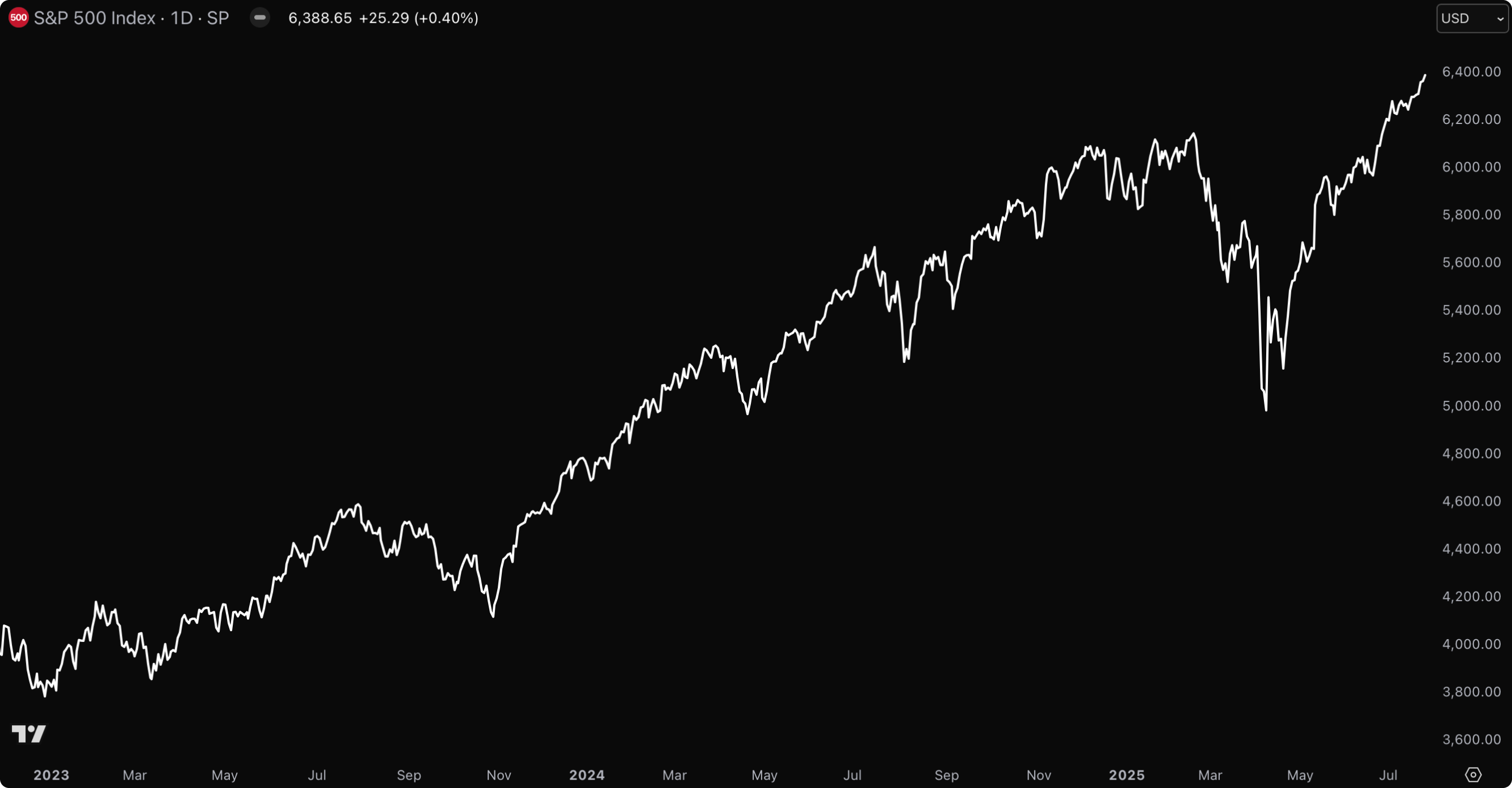

🇺🇸 S&P 500 rallied 1.46% to another all-time high. One of the big themes this year has been the European outperformance of US stocks, but that ended this week with the S&P 500 flipping the STOXX 600 in year-to-date performance. The two indices are now up 8.62% and 8.34% respectively.

🇺🇸 Nasdaq Composite lagged the S&P but still gained 1.02% and closed at a new all-time high. The Nasdaq is now up 42.5% from the April lows and 9.31% for the year.

🇺🇸 Dow Jones Industrial rose 1.26% to its second highest weekly close in history, just barely below its prior all-time high from November of last year.

🇺🇸 Russell 2000 gained 0.94% for the week but is still more than 8% off its peak.

🇨🇦 TSX just continues to grind higher in an impressively stable uptrend, adding 0.66% this week for its eighth weekly all-time high in just 11 weeks.

🇲🇽 IPC rallied 1.87% for the week after having been down as much as 1.74% on Tuesday.

🇧🇷 Bovespa eked out a 0.11% gain but closed at the bottom of its intraweek trading range.

🇦🇷 Merval saw a massive surge of 5.87% for the week, despite dropping more than 3% during Monday and Tuesday.

Europe

🇪🇺 STOXX 600 gained 0.54% this week but was still overtaken by the S&P 500 in year-to-date performance.

🇬🇧 FTSE 100 jumped 1.43% to another all-time high and extended its gain for the year to 11.59%.

🇩🇪 DAX continues to consolidate near its all-time high, inched down by 0.3% this week.

🇫🇷 CAC 40 eked out a 0.15% gain for the week.

🇩🇰 C25 vaulted 3.18% after four weeks with minor movements. The big gain was largely driven by strong rallies in Novo Nordisk and Maersk.

Asia

🇯🇵 Nikkei 225 soared 4.11% to a new all-time high weekly close, surpassing its peak from a year ago.

🇨🇳 Hang Seng jumped 2.27% to another cycle high, closing at levels not seen since November 2021. The Hang Seng is now up more than 26% on the year.

🇮🇳 Nifty 50 declined 0.53% for the week.

🇰🇷 KOSPI eked out a 0.25% gain in its third week of sideways consolidation after a massive 39% run-up from the April lows.

🇹🇼 TSEC inched down by 0.08% this week.

Currencies & Commodities

💰 The DXY failed to continue its rebound and declined 0.8% this to 97.674 week.

🇪🇺 USD.EUR dropped 1.06% to 0.8517 EUR.

🇩🇰 USD.DKK declined 1.03% to 6.3528 DKK.

🇬🇧 USD.GBP inched lower by just 0.12% to 0.744 GBP.

🇯🇵 USD.JPY weakened by 0.77% to 147.65 JPY.

🇨🇳 USD.CNH inched down by 0.19% for the week after hitting a new 8-month low on Thursday.

🥇 Gold rallied to begin the week but staged a reversal on Wednesday, closing the week down by 0.4% at $3,336 per ounce.

🥈 Silver saw similar price action as gold but ended the week virtually unchanged.

🥉 Copper was the big outperformer, rallying 4.12% this week to yet another all-time high.

🏆 Bitcoin is flat for the week at $117,400 as of Saturday morning (CET) after trading in a relatively tight range of $114,700 to $120,300 throughout the week.

The altcoin market is taking a breather after last week’s massive jump, losing around 1.75% as of Saturday morning. The big laggard is Ripple (XRP) with a 8.5% decline while Binance Coin (BNB) and Solana (SOL) are outperforming with 3.4% and 2.8% gains.

Bond yields

🇺🇸 The US 2-year has gained 1.34% and is back above 3.9%.

🇺🇸 The US 10-year fell 0.77% this week to a yield of 4.386%.

🇺🇸 The US 30-year once again backed off of the 5% level and dropped 1.28% for the week.

🇪🇺 The Euro 2-year jumped 4.86% to a yield of 1.922%, its highest level since March.

🇪🇺 The Euro 10-year rose 1.12% to 2.708%, also a 4-month high.

🇨🇳 The China 10-year rallied 3.7% to a 1.736% yield, the highest since pre-Liberation Day.

🇨🇳 The China 30-year surged 4.03% and briefly surpassed 2% for the first time since March.

Other

The VIX fell 9% this week and closed below 15 for the first time since February. The stock market is now just as calm as before the whole tariff debacle began.

.png)